Republicans want to get Democrats on record on the costly rules

House Republicans have teed up a vote this week on legislation to block President Biden’s back-door electric-vehicle mandate. Democrats are spinning the legislation as an attack on public health, innovation and free markets. The debate is a preview of what we can expect in the 2024 election campaign.

The Environmental Protection Agency “is not imposing an EV mandate,” says a memo from Democrats on the Energy and Commerce Committee opposing the GOP legislation. But the EPA in April proposed tailpipe emissions standards for greenhouse gases that would effectively require that electric vehicles make up two-thirds of car sales in 2032.

The only way auto makers could meet the emissions restrictions is by producing more EVs and fewer gas-powered cars. This is a mandate in everything but name, and it’s already causing enormous problems.

The House GOP bill would prohibit EPA from finalizing its proposed CO2 emissions standards and bar any regulation that would “mandate the use of any specific technology” or “result in limited availability of new motor vehicles” based on the type of engine. This means EPA couldn’t promulgate a similar new mandate.

The Democratic memo accuses Republicans of attacking “EPA’s authority to protect Americans from dangerous air pollution.” But greenhouse gases are ubiquitous and aren’t hazardous to human health, unlike tailpipe pollutants such as sulfur dioxide and particulate matter. Some studies suggest EVs may produce more fine particulate matter—pollutants that lodge deep in the lungs—because their battery weight increases wear and tear from tires. EPA ignores this potential harm.

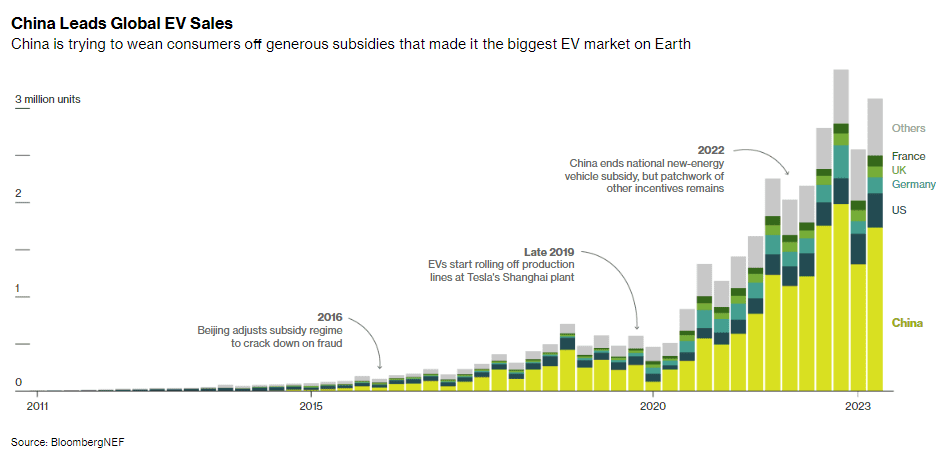

“American demand for EVs is already outpacing supply,” the Democratic memo says, and “auto manufacturers are independently trending toward EVs because of increasing popularity with consumers.” Then why are auto makers scaling back EV production plans? And why are thousands of auto dealers begging the Administration to tap the brakes on the EPA regulation as EVs pile up on their lots?

Telsa accounted for nearly two-thirds of EV sales last year. Battery-powered EVs make up less than 3 percent of most auto makers’ fleets, which means they’d face an extremely steep ramp-up to hit the 2032 mandate. Even with Inflation Reduction Act subsidies, the Energy Information Administration forecasts that EVs will make up only 15 percent of sales in 2030.

That means auto makers will have to raise prices on gas-powered cars to offset losses on EVs they are required to make to meet government quotas. Ford lost $62,016 for every EV it sold in the third quarter. The only alternative is to buy regulatory credits from EV manufacturers. Tesla pocketed about $2,380 in credit sales for each car it sold in the U.S. during the first six months.

Democrats say the GOP legislation would “stifle innovation,” but car makers could continue to improve battery technologies. They merely wouldn’t be forced to lose money mass-producing EVs for consumers who don’t want them. Why can’t Democrats let producers meet the market demand for consumers?

As the facts about Mr. Biden’s EV mandate become better known, and the implications for consumers sink in, it is going to be an issue in 2024. If EVs were as popular as the climate lobby claims, the Administration wouldn’t have to mandate them, and Democrats wouldn’t be dissembling about what they’re doing.