The US auto market defied expectations for a slowdown by eking out another quarter of sales growth. But the high cost of financing drove Americans to opt for more affordable models.

Budget sedans and compact SUVs from Toyota Motor Corp. and Honda Motor Co. made eye-popping share gains in the first quarter, according to researcher Edmunds.com. Large pickup trucks – one of the industry’s priciest segments – lost ground in January and February, according to researcher GlobalData. Several brands, including Jeep, Tesla and Ford, reduced prices to win back inflation-weary consumers and spur demand in the sluggish electric vehicle market.

“I’m surprised about how resilient the market has been,” said David Oakley, an analyst with GlobalData. “Affordability is a massive issue for the industry, and it will be going forward. But right now it seems they’re weathering the storm, and people are somehow making it work.”

Global automakers, including Toyota and General Motors Co., will offer more insights when they release first-quarter sales results Tuesday, while Ford Motor Co. reports on Wednesday.

The industry’s yearly sales pace, known as the seasonally adjusted annual rate, rose to about 15.8 million in March, up from 14.9 million a year ago, according to the average estimate of eight analysts surveyed by Bloomberg. The 3.8 million vehicles sold in the first quarter mark a 6 percent increase from a year ago, but a 3.1 percent drop from the final quarter of 2023, Edmunds said.

The pricing bonanza that juiced automaker profits during the pandemic is fading as production normalizes and the highest interest rates in more than two decades damp demand. Now that inventories are rising, car companies are doling out more incentives and prices are starting to slip.

Consumers seem to be cooling to fully electric vehicles due to a lack of charging infrastructure and high prices. While EV sales rose from a year ago, volume in the first quarter likely declined sequentially for the first time since early in the pandemic, according to researcher Cox Automotive. Meanwhile, sales of hybrid vehicles, which offer good fuel economy and sticker prices that are closer to their gas-powered siblings, are growing.

Steve Gates, a dealer who owns ten stores across Kentucky, Tennessee and Indiana, said sales in the first quarter were better than he expected considering affordability is still weighing on shoppers. That’s especially true for hybrids. In a sign of the financial strain on consumers, he can’t acquire enough used cars to meet demand from shoppers who’ve been priced out of new models.

“The demand is still there,” said Gates, who sells several brands, including Toyota, Lexus and Ford. With just the plug-in version of Toyota’s RAV4, “I could make a living if I could just get those things and nothing else.”

Other dealers warned that high borrowing costs have divided the new-car market into haves and have-nots: Affluent shoppers can swallow average financing costs that have risen to 7 percent while many other potential buyers balk. The average monthly payment on a new car rose to a record $747 in February, up roughly 25 percent from three years ago, according to Edmunds.com.

The financial pain is especially acute for people who bought new vehicles from 2021 to 2022, when supply-chain snarls and vehicle shortages allowed dealers to charge more than manufacturers’ sticker prices. Many of those buyers are now saddled with underwater car loans as vehicle prices normalize. That’s another potential drag on sales of new models, said Jessica Caldwell, executive director of insights at Edmunds.

The growth of electric cars and unwinding of price gains ignited by low inventory during the pandemic created uncertainty in the market because there isn’t a clear historical precedent for what’s happening, Caldwell said.

“A lot of people just made snap purchase decisions because cars were flying off the lots” during the pandemic, she said. “All of a sudden, you find yourself in an unfavorable financial situation.”

The electric car revolution is losing its charge

In the electric-vehicle race, it’s increasingly clear that not every competitor will make it to the finish line.

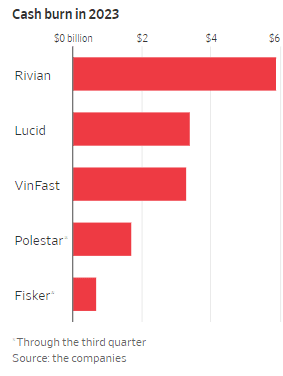

Companies like Rivian Automotive, Lucid Group and Fisker are burning through their cash reservers as they spend heavily on expanding factory production and sales – all while losing money on every vehicle they sell.

For consumers, the increased competition translates into steep discounts on some of the flashiest electric-powered vehicles. But for EV automakers, a slowdown in demand starts the clock that might determine how long they can keep the lights on.

Many of these companies first unveiled a lineup of innovative battery-powered cars and SUVs in 2018 and 2019, following Tesla’s pioneering success in the new market. It seemed like an army of upstarts was poised to supplant stodgy giants such as Ford Motor and Toyota as the next household name in the industry.

Electric cars were just starting to break into the mainstream, and sales of Tesla’s popular Model 3 sedan were taking off.

These young companies went public at stratospheric valuations, even though many had no revenue and little experience building a car. Investors, analysts and ordinary shoppers believed EV makers could emulate Tesla’s success in disrupting the traditional car market. Rivian’s market value briefly surged higher than that of Ford or General Motors.

Now, these companies are fighting to stay afloat amid stiff competition. Sales of battery-powered cars and trucks have been weaker than expected in the U.S., leading companies from Ford to Tesla to slash prices in an attempt to jump-start demand. Too few buyers have been willing to make the switch to fully electric vehicles, worried about the relatively high sticker prices, still-nascent charging infrastructure and the long-term reliability of EVs. Money-losing startups are pulling back on spending and delaying investments as they seek to conserve their remaining cash.

Some, like electric-pickup maker Lordstown Motors and battery-powered van company Arrival, have already filed for bankruptcy, and others are producing only a trickle of vehicles.

These carmakers that went public in an era of low interest rates and rising buzz around electric vehicles now have to prove they can withstand tougher conditions. They say they are focused on stabilizing their cash-bleeding operations, but not all of them may be able to weather the storm.

Here’s our guide on who could survive the battle of the fittest, using battery icons* to signify financial health.

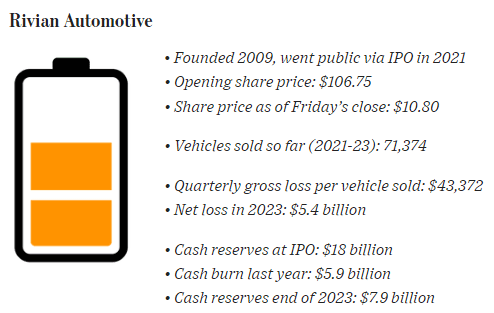

Vehicle Lineup: Rivian currently sells the R1T pickup and R1S SUV, which start at $69,900 and $74,900, respectively. The company also builds an electric commercial van for Amazon.com

Sales Pitch: Often compared to the clothing brand Patagonia, Rivian targets affluent, climate-conscious adventure seekers. Company founder RJ Scaringe has said he wanted to build an electric pickup because it is the most popular type of vehicle sold in the U.S.

How It Got Started: Scaringe, an avid outdoors lover, started the company in 2009, mortgaging his home for startup funds. Rivian raised billions privately from investors such as Amazon and Ford before going public in one of the most lucrative IPOs of the past decade. The company purchased a former Mitsubishi Motors factory in Normal, Ill., in 2017 to build its first vehicles.

Quirks of the Vehicles: Rivian’s vehicles have features meant to be useful off the beaten track, such as “camp mode” that levels the vehicle on an incline for comfortable in-car camping and a portable speaker stowed under the center console.

What Happened: Supply-chain logjams and problems getting parts to the assembly line meant that Rivian struggled to operate its factory at maximum capacity. The manufacturing challenges contributed to the company burning around $1.5 billion a quarter. The company also had to redesign key parts of its vehicles in an attempt to bring production costs down. While Rivian was able to overcome many of the logistics snarls holding up its factory output, the company is now warning of weaker demand for its models.

Where Are They Now? Rivian is still losing money each quarter and faces immediate challenges in meeting its goal of generating gross profit by the end of the year. The carmaker loses tens of thousands on every vehicle it sells, but executives say those losses are expected to decline this year. Rivian said it plans to build roughly the same number of vehicles this year as last.

Ultimately, Rivian aims to become one of the world’s largest carmakers. The first step in that plan is a new, $45,000 SUV called the R2, which it unveiled this month and is to go on sale in 2026. The company says this model is key to transforming into a profitable EV maker.

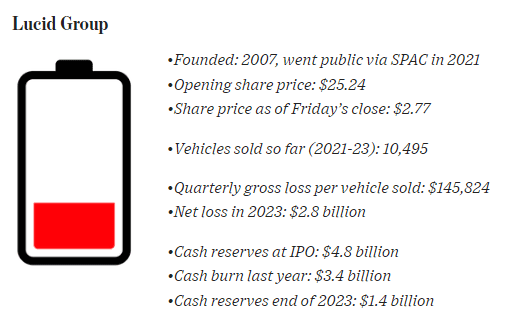

Vehicle Lineup: Lucid currently sells one model, the Air sedan, which ranges in price from the $69,900 Air Pure to the $249,000 Air Sapphire. An SUV, called the Gravity, is due to go on sale later this year.

Sales Pitch: Lucid sold investors on a plan to build high-end battery-powered vehicles, fueled by what it calls “the best electric-vehicle technology.” The company’s battery and electric-motor technology allow it to squeeze out more mileage than its competitors. Even the cheapest version of Lucid’s Air sedan can travel 410 miles on a single charge, around 100 miles farther than most electric vehicles available in the U.S.

How It Got Started: Lucid started life at a battery venture called Atieva. That company’s founders in 2013 hired Peter Rawlinson, a former Tesla executive, who was brought in to help Atieva pivot to car manufacturing. In 2016, Atieva changed its name and Lucid was born. When the company started to run out of cash in 2018, a $1 billion investment from the Saudi Arabia Public Investment Fund saved it. Rawlinson became chief executive in 2019.

What Happened: At first, Lucid appeared to have a deep well of demand, reporting more than 25,000 reservations for the Air in early 2022. With a factory in Casa Grande, Ariz., Lucid seemed both well-funded and well-prepared. Instead, sales have been relatively flat since the second half of 2022. Lucid began flagging slower demand for the Air last February—sooner than other startups on this list. In response, the company has been spending more on marketing and cutting prices to help boost demand.

Where Are They Now? Lucid’s newest factory in Saudi Arabia is currently assembling vehicles as part of a deal to sell at least 50,000 to that country’s government. The company is also slated to start production of the Gravity this year. Company executives say the vehicle will appeal to a wider audience, because SUVs outsell sedans three-to-one in the U.S. Lucid also says it is preparing to broaden its lineup further in 2026, when it plans to launch a new, more affordable midsize vehicle.

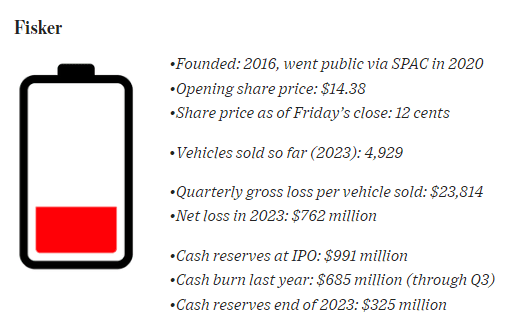

Vehicle Lineup: Fisker currently sells the Ocean SUV, which costs between $38,999 and $61,499.

Fisker’s Sales Pitch: Fisker has taken a different approach than other startups, employing what it calls an asset-light business model. Rather than building the cars itself, it contracts that work out to an outside company. That way it doesn’t have to own a factory itself or employ a manufacturing workforce.

How It Got Started: This is the second electric-car startup started by former BMW and Aston Martin car designer Henrik Fisker, who is also CEO. His first company, Fisker Automotive, sold a $100,000 plug-in hybrid called the Fisker Karma, but it went bankrupt in 2013 after 300 vehicles were destroyed in a hurricane and its battery supplier went out of business.

Four Unique Features: “Each Fisker has to have at least four unique features that have to be either best-in-class or something nobody else has,” says the Fisker CEO. The features include the Fisker Ocean’s “California mode,” which opens every glass panel, except the windshield, and a small foldout shelf dubbed the taco tray. The company’s forthcoming Alaska pickup truck has a “cowboy hat holder” and “the world’s largest cup holder.”

What Happened: Fisker only started delivering vehicles to customers halfway through 2023 after missing self-imposed deadlines. The company says it ran into delays securing parts and regulatory approval. As a result, it slashed its production outlook twice last year, but ultimately fell short of even its reduced goals.

Where Are They Now? Fisker warned at the end of February that it risked running out of cash this year. As of mid-March, the company had nearly 5,000 unsold vehicles and its cash reserves had dwindled to $89 million. Fisker says it is raising $150 million in fresh funds from an investor and is negotiating with a large carmaker for another investment. Fisker has hired restructuring advisers to help prepare for a potential bankruptcy filing, according to people familiar with the matter.

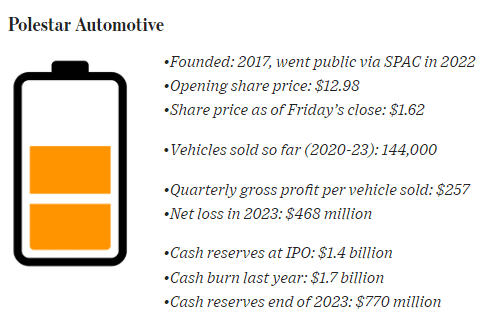

Note: Gross profit per vehicle, net loss and cash burn are as of end of September, 2023, because the company has yet to release full-year results.

Vehicle Lineup: The carmaker sells three models: the $49,200 Polestar 2 sedan, $73,400 Polestar 3 SUV and approximately $60,000 Polestar 4 SUV.

Sales Pitch: Like Fisker, Polestar doesn’t own manufacturing facilities, and instead contracts to have its vehicles built at other companies’ factories in China, South Korea and the U.S. Unlike most electric-car makers, Polestar says it doesn’t want to make a mass-market EV. Instead, the company pitches itself as a sportier alternative to Volvo.

How It Got Started: Volvo Car and its Chinese parent, Geely, created Polestar as an EV-only brand in 2017. The company started by selling a hybrid, the Polestar 1, before launching the fully electric Polestar 2 in 2020.

Quirk: Polestar vehicles bear more than a passing resemblance to electric vehicles made by Volvo. That may not be surprising given that the CEO, finance chief, operations head and lead designer are all former Volvo executives.

What happened: Polestar appeared to have the smoothest launch of any of the current crop of EV startups. It has built over 100,000 vehicles since starting production and has even turned a profit in some quarters. But Polestar has faced slowing demand for its Polestar 2 sedan and the launch of its Polestar 3 SUV was delayed after Volvo ran into software development issues. The company has slashed its production outlook and Volvo said last month that it will sell the majority of its 48% stake in Polestar.

Where Are They Now? Polestar’s finances are now stable after raising nearly $1 billion in debt last month. Production of the Polestar 3 has started in China, and a U.S. plant is due to start producing the vehicle later this year. Polestar’s chief financial officer says the company is targeting a double-digit gross margin by the end of 2024. The company says the U.S. launch of the Polestar 3 SUV this year will help boost sales.

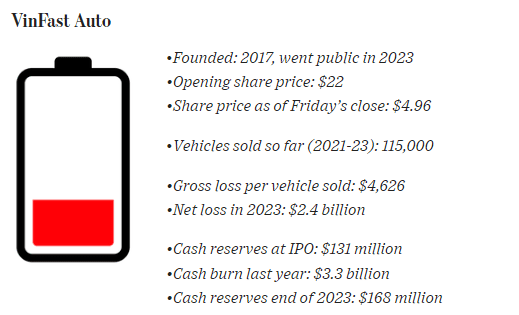

Vehicle Lineup: In the U.S., VinFast currently sells the $46,000 VF8 SUV. A larger SUV called VF9 is expected to go on sale this year, starting at $79,800. VinFast also sells battery-powered scooters in Vietnam.

How It Got Started: VinFast was created in 2017 by Pham Nhat Vuong, the billionaire owner of Vietnamese conglomerate Vingroup, which operates a diverse array of businesses from hospitals to theme parks. VinFast built a massive $1.5 billion factory east of Hanoi, which the company has said will be capable of producing nearly a million vehicles a year by 2026.

VinFast’s Sales Pitch: VinFast aims to compete with Chinese EV startups like BYD and NIO, and says that building cars in Vietnam means its labor costs are even lower than those of Chinese competitors. The company is expanding across Southeast Asia and in India, while also aiming to increase its sales in the U.S.

Quirk: Early buyers in the U.S. were offered free stays in one of Vingroup’s resorts in Vietnam. People who buy a home in Vietnam from the company’s property arm may also get a free car as part of the deal.

What Happened? VinFast tried an innovative pricing strategy in which it sold cars to customers but rented the lithium-ion batteries that power the vehicles separately. The company said the plan allowed customers to pay less upfront for VinFast vehicles, but ended up ditching the plan in the U.S. for now, because customers found it confusing. Ultimately, VinFast only delivered a little over 3,000 vehicles to U.S. customers last year, according to Motor Intelligence.

The company also had a rocky debut on Wall Street. Initially, its share price skyrocketed, briefly making VinFast more valuable than Ford or GM, in part because only a small percentage of the company’s shares were available for trade, boosting demand for them. Since then, the stock price has tanked as the company faced challenges getting its first batch of cars to U.S. consumers. Reviewers panned the VF8 for quality issues.

Where Are They Now? VinFast is building a $2 billion factory in North Carolina, which will allow its vehicles to potentially qualify for a federal tax credit. Over 70% of VinFast’s passenger vehicles and nearly half of its scooter sales last year were to a taxi company owned by Vuong, the head of Vingroup. VinFast has said it plans to deliver 100,000 electric cars and SUVs this year, but hasn’t said how many will be to customers outside of the Vingroup network.

* NOTE: A fully charged battery would signify a profitable, cash-generating business. Two bars of charge denotes a company draining its cash reserves but has more cash on hand than it spent last year. A company whose cash burn last year was greater than the sum of its current cash and cash equivalents is assigned one bar of charge.

To avoid hefty tariffs, China’s BYD eyes U.S. car market via Mexico

Chinese automaker BYD has set its sights on Mexico as its quest for global expansion turns toward North America.

The Shenzhen-based car company, whose rapid growth has made it one of the world’s largest electric-vehicle sellers, is scouting locations in the country for a factory, from which it would consider exporting cars to the U.S., according to people familiar with the matter.

The plans show rising enthusiasm within China’s car industry for expansion to North America, despite the political risks. Building cars in Mexico for the U.S. would allow the automakers to avoid hefty import tariffs that would be applied if they were to send them directly from China.

CEOs at rival automakers have warned about the potential threat from China, with some suggesting the need for more government action to avert such competition in the U.S. These executives are concerned about what they see as a big cost advantage enjoyed by their Chinese competitors in EVs.

Any such clash could still be some time away, and people familiar with BYD’s plans said it hasn’t made any decisions about Mexico.

A BYD spokesperson said the company doesn’t have any “imminent announcements to make regarding new markets.”

At least a dozen Chinese electric-car component suppliers have announced new factories or added to their existing investments in Mexico in recent years, according to stock-exchange filings. These parts makers are responding to a U.S.-Mexico-Canada trade deal that encourages carmakers in North America to use locally sourced content.

The most competitive automakers

BYD, short for Build Your Dreams, has been rapidly expanding both inside and outside China. In recent years, BYD’s low-price EVs have gained traction with buyers in places such as Europe and Southeast Asia.

In recent weeks, executives at some Western car companies have become more vocal about the potential threat these Chinese firms pose to their own EV plans. Through a mix of engineering, government subsidies and lower labor costs, BYD and other China-based EV makers have been able to lure customers with stylish and technologically advanced EVs at attractive prices.

On Thursday, Carlos Tavares, chief executive of Chrysler-parent Stellantis, said it was imperative the global automaker be able to match its Chinese rivals on cost, or it would risk ceding ground. He described their expansion as “very powerful” and likened their potential entry in the U.S. to the arrival of the Japanese automakers in the 1970s and South Korean firms in the 1990s.

“You can see it in the European markets,” Tavares said during a conference call with analysts. “We may not want to see—a third time—the same movie.”

Tesla Chief Executive Elon Musk has also expressed similar concerns, saying the Chinese companies have already had significant success outside of China and are now the “most competitive” in the world.

“If there are not trade barriers established, they will pretty much demolish most other car companies in the world,” Musk said, during Tesla’s earnings call in January.

The European Union is conducting an investigation of Chinese EV makers that could result in new tariffs if EU officials find the Chinese companies are receiving unfair subsidies.

Benefits of Mexico

Mexico would be a natural staging point for Chinese automakers to enter the U.S. market because of its proximity, relatively low labor costs and the opportunity to take advantage of low or zero tariffs on made-in-Mexico vehicles. People familiar with BYD’s plans said some of the locations it is examining are near the U.S. border.

Currently, Chinese-built EVs are subject to a 27.5 percent tariff when imported into the U.S.—the regular 2.5 percent tariff that generally applies to imported cars plus an additional 25 percent tariff that hits Chinese-made cars and was introduced by the Trump administration in 2018.

The Biden administration is debating whether to raise tariffs on Chinese EVs further, The Wall Street Journal has reported, and has also limited eligibility for a $7,500 consumer subsidy for cars built with batteries made by Chinese companies.

Cars made at a Chinese-owned factory in Mexico, by contrast, could enjoy the low 2.5 percent tariff upon entering the U.S. The factory’s cars could possibly pay no tariff if they met stringent standards for local content under the U.S.-Canada-Mexico Agreement adopted in 2020.

Executives at Toyota in North America estimated in an internal memo last fall that Chinese companies had a 25 percent to 30 percent cost advantage over global competitors when manufacturing EVs—more than enough to overcome the small U.S. tariff. If the U.S. government pushes EV adoption too quickly, it would serve as an open invitation for Chinese EV companies including BYD, Geely and NIO to “storm the U.S. market,” the memo said.

Stella Li, a top BYD executive, visited Mexico City in January to discuss the car maker’s expansion plans in Mexico with local officials, the country’s economy ministry said. BYD recently appointed Jorge Vallejo, who formerly worked for Nissan and Mitsubishi in Mexico, as its general director in the country.

U.S. monitoring investments

At home in China, BYD makes many parts in-house, including its EV batteries, to reduce costs. It isn’t clear how much BYD would be able to replicate those cost advantages by shifting some production to Mexico.

Although BYD executives have long harbored ambitions to sell passenger EVs in the U.S., they have moved cautiously given the potential backlash from regulators and U.S. rivals. In North America, the company currently sells electric buses and trucks made at its site in Lancaster, Calif.

As BYD weighs the possibility of selling cars to Americans, the coming U.S. presidential election is one factor it is watching closely, people at the company said. BYD executives see other potential uses for the plant in Mexico, including using it as an export hub for shipping cars to South America or sending batteries and other car parts to the U.S. Japan’s Nikkei newspaper earlier reported that BYD was looking at a plant in Mexico.

Officials in the Biden administration are monitoring Chinese investment in Mexico amid concerns Chinese businesses could take advantage of North American free-trade agreement rules. In December, Treasury Secretary Janet Yellen visited Mexico to strengthen cooperation on security and financial issues, including plans to establish a group to review foreign investments in North America.

“There’s no question the global expansion of the Chinese auto industry is a highly disruptive force,” said Matt Blunt, president of the American Automotive Policy Council, an auto-industry lobbying group that counts

“We don’t have a specific policy prescription, but we think it’s important that industry leaders and policymakers are thinking about the potential implications,” he said.

Cincinnati trails its peers, Milwaukee, Nashville, when it comes to dealers offering EVs

Sales at traditional dealerships lag behind similarly sized cities such as Milwaukee, Nashville

Nationwide, 55 percent of new car dealers are selling electric vehicles, while in Cincinnati, that number is 48.2 percent, according to ISeeCars.com, an online automotive search engine and research website. That puts Cincinnati at No. 92 out of 132 metro areas. The figures exclude Tesla stores.

When it came to growth in the number of new car dealers selling electric vehicles, Cincinnati ranked 129th.

Legendary Cincinnati car dealer Jeff Wyler said the demand has not been there.

“There’s a lot of talk about electrics,” Wyler told the Business Courier last year. “And the electrics are not selling. They’re just standing on the lots. So it appears that our government is trying to force electrics on consumers, and consumers aren’t buying yet.”

The story for used car dealers is a bit different. Nearly 32 percent of local used car dealers are selling electric vehicles, putting the region 33rd in the country.

In terms of growth rate, Cincinnati ranked 98th.

Still, selling electric vehicles as a mass market product is relatively new. Before 2021, only 16.5 percent of non-Tesla new car dealers were selling electric vehicles. Larger dealers are more likely than smaller dealers to have them. And three years ago, most brands did not offer an electric vehicle.

ISeeCars analyzed the inventories of new and used car dealers to produce this data. Non-Tesla electric vehicles comprise about 5 percent of all U.S. vehicle sales, up from 0.5 of a percent in 2020.

Cincinnati lags behind other similarly sized cities. In Milwaukee, 72.5 percent of new car dealers sell EVs, while 64 percent do in Kansas City and 66 percent do in Nashville. All three of those peer cities are in the top 10 nationwide.

Karl Brauer, an executive analyst for ISeeCars, said Cincinnati likely trails other cities for a number of reasons: weather, economic circumstances, cost and conservative politics.

“You have people who will not buy an electric vehicle under any circumstances. You have people who that’s all they’ll buy,” Brauer said. “EVs can be a tougher sell in colder climates because of the reduced range and performance when it gets cold. You can’t blame the dealers or the residents for being hesitant. Economic circumstances can play a role. If you’re looking at two similar vehicles … the electric will cost more.”

Greg Joseph with the Joseph Auto Group said people should not think Cincinnati dealers don’t have EVs for sale. In reality, it’s been about a year since non-Tesla EVs came into the mainstream, so nobody should expect them to make up a high volume of sales at this point. Customers are interested in them and asking about them, and Joseph believes the EV segment will continue to grow locally.

So-called mileage or range anxiety also is a factor. It takes 10 minutes for someone to go to a gas station and fill their car with gas. The same process with an electric vehicle could take an hour, depending on the location of the station, whether there’s a line to use it and what kind of charging infrastructure it has.

“It currently is the No. 1 issue with electric cars. I think it will be the hardest one to overcome,” Brauer said. “If you want to have electric cars as dominant, you have to do more.”

Cincinnati Business Courier Region’s Hottest Selling Vehicles

Rank

Make / Model

One year change in sales

Number sold in 2023*

1

Honda Civic

+12.9%

4,280

2

Chevrolet Equinox

-6.3%

3,841

3

Ford F-150

-2.6%

3,730

4

Honda CR-V

-6.2%

3,006

5

Honda Accord

-2.5%

3,003

6

Chevrolet Silverado 1500

+13%

2,902

7

Toyota Camry

+14.8%

2,839

8

Ford Escape

+1.2%

2,659

9

Toyota RAV4

+6.1%

2,267

10

Chevrolet Malibu

-14.6%

2,129

11

Toyota Corolla

+10.6%

2,014

12

Ford Explorer

-0.7%

2,016

13

Honda Odyssey

+20.2%

1,921

14

RAM 1500

+1,500%

1,872

15

Nissan Rogue

+2.1%

1,810

16

Chevrolet Trax

+82.4%

1,809

17

Chevrolet Traverse

+12.3%

1,722

18

Honda Pilot

+2.7%

1,659

19

Ford Fusion

-11.3%

1,654

20

Mazda CX-5

+8.1%

1,598

21

Nissan Altima

-21.9%

1,571

22

Hyundai Elantra

+21.3%

1,515

23

Jeep Grand Cherokee

+10.4%

1,455

24

Kia Forte

+4.8%

1,409

25

Hyundai Sonata

-3%

1,362

*Includes Butler, Clermont, Hamilton and Warren counties

GM Went all in on EVs. Dealers say buyers want hybrids

Some auto retailers worry GM is missing an opportunity to nab buyers who aren’t ready for EVs

Some influential dealers are pressing General Motorsto introduce hybrid models, worried they risk losing customers who aren’t ready to make the switch to fully electric cars.

Dealers who serve on advisory committees to the automaker have urged executives in several recent meetings to add hybrids to GM’s lineup, according to people involved in the discussions. GM has focused on fully electric cars in recent years and largely bypassed hybrids, which pair an internal combustion engine with a small battery and electric motor to boost fuel efficiency.

The dealers said they expressed concern that more customers are looking for a middle ground between conventional gas-engine cars and EVs, which are more expensive and require regular charging.

GM executives have acknowledged the dealers’views but haven’t made any commitments to future hybrid options, the people said. Automakers often solicit input from dealers on vehicle planning but still typically keep the details of future models under wraps.

A GM spokesman declined to comment.

The dealers’ pleas for the company to consider adding hybrid models show another dimension of the pressure facing GM Chief Executive Mary Barra as aspects of her EV push stall.

Making such a move would mark a major strategic reversal for GM, which unlike many of its rivals, went all-in on EVs and largely sat out the hybrid market, which executives viewed as an unnecessary interim step.

Last month, Barra didn’t rule out the prospect of introducing hybrid models in the U.S. when asked about it during an event in Detroit, noting that GM sells them in China.

“I still believe in the endgame, that you want to move to EVs as quickly as you can,” she said. “But we have the technology, and we’ll continue to look at where the market is.”

Meanwhile, hybrids have taken off over the past year amid consumer reticence toward full electrics, turned off by higher prices and worries about getting stranded between charging stations. Many dealers and car executives see hybrids as an important choice on the spectrum between straight gas-powered cars and EVs.

Toyota, Honda, Hyundai and Kia are the major players in the hybrid market. Sales of hybrid vehicles in the U.S. surged more than 50% last year, after a small drop in 2022, according to research firm Motor Intelligence.

Those include regular hybrids, which supplement the gas engine but generally don’t propel the car on electric power alone, and plug-in hybrids, which can travel in electric mode for a certain distance—typically 10 to 40 miles—before the gas engine takes over.

“Hybrids are what’s hot right now,” said Chris Hemmersmeier, a Salt Lake City-area car dealer who has GM stores as well as other brands, including Kia and Jeep.

He said hybrid models at those non-GM stores—including the Kia Sportage compact SUV and Stellantis’s Jeep Wrangler and Grand Cherokee plug-in-hybrid SUVs, sold under the 4xe name—have been selling briskly, and he’s worried GM’s EV-heavy focus will cause his stores to lose customers.

“I’d like to see GM prioritize hybrids,” said Hemmersmeier, who operates Chevrolet and Buick-GMC stores and hasn’t been involved in the dealer-committee meetings with company executives.

GM offered hybrids for the U.S. market at times over the past two decades. In the mid-2000s, it came out with hybrid versions of its big SUVs, such as the GMC Yukon and Cadillac Escalade, among its most profitable vehicles. Those sold poorly, though, and were phased out within a few years.

GM was among the first automakers to introduce a plug-in hybrid when it released the Chevrolet Volt in 2010. It offered about 40 miles of driving range in electric mode before a gas generator kicked on to power the electric motor. The Volt was celebrated as an engineering feat and garnered a loyal following, but was a money loser and fell short of GM’s internal sales targets. The company discontinued it in 2019.

Today there are dozens of plug-in hybrid models on sale in the U.S., with Stellantis’s SUVs the top sellers.

In recent years, GM executives have expressed skepticism about hybrid technology and concern that they would distract from the company’s long-term goal of near-exclusive electric sales by 2035.

“Customers generally aren’t interested in hybrids, the value proposition there,” Barra said at a Barclays investor conference in 2019. “We believe moving to electric vehicles as quickly as possible is the right thing to do.”

In recent months, dealers more broadly have expressed worries that U.S. policy to expand EV adoption is getting ahead of consumers.

Last week, auto retailers representing about 5,000 U.S. stores sent a letter to President Biden, urging his administration to stand down from proposed new tailpipe-emissions rules that would require more than half of U.S. sales to be EVs by next decade. They said a lack of charger availability and consumer interest make that unrealistic.

“Wait for the American consumer to make the choice to buy an electric vehicle, confident that they are affordable and won’t strand them because of a lack of charging stations,” the letter said.

Used-car market normalizing, though affordability, inventory concerns remain

Dealers are assessing what the return of new-vehicle supply and used-vehicle depreciation means for demand in 2024

Pent-up demand for used vehicles remains strong at the start of 2024, though dealers plan to closely monitor how a gradually normalizing new-vehicle market influences that throughout the year.

Of increasing concern for dealers is how much automakers with revived new-vehicle supply push for and incentivize new-vehicle sales in certain segments — and how that trickles down to impact used-vehicle demand.

Jim Farkas, general manager of Germain Honda of Ann Arbor in Michigan, told Automotive News that with automakers starting to be more aggressive on new-vehicle sales, dealers need to strike a balance between new- and used-vehicle inventory and stay efficient in turning the used vehicles.

“I’m having our used-car management staff make sure they’re talking to new-car managers and understanding the supply and demand,” Farkas said.

An oversupply of new vehicles would affect used-vehicle prices, he said.

“This would be due to the manufacturer noticing the supply growing, then offering incentives,” said Farkas, who also is used-car director for Germain Motor Co., which ranked No. 58 on Automotive News‘ list of the top 100 dealership groups by used-vehicle sales in 2022. “Whether it’s a value incentive, such as cash or rebates or APRs, [that] will have an impact on used-car sales, which will of course force them to decline in price.”

The extent of that influence on pricing will vary, he said, since supply of each brand is “totally different.” Stellantis dealerships, for instance, generally have more new-vehicle days’ supply than Honda or Toyota dealerships do right now, he said.

Nathan Myers, used-vehicle director for Sons Auto Group of Atlanta, said his group will be cautious this year about stocking an overabundance of new-vehicle inventory in certain segments, such as full-size pickups.

Dealers didn’t have to think much about that in 2021 when few new vehicles were on the ground because of the shortage of semiconductors during the COVID-19 pandemic, he said.

“I think you’re going to see that come up with every manufacturer” in 2024, Myers said. “It’s just going to be [a matter of] to what extreme.”

Shift from seller’s market

Cox Automotive expects a semblance of balance to return to the U.S. market in 2024, particularly on the used-vehicle side.

Wholesale used-vehicle prices are decreasing more consistently, Cox said. On a mix-, mileage- and seasonally adjusted basis, they fell 0.5 percent in December from November, according to the firm’s Manheim Used Vehicle Value Index. That is down 7 percent from one year ago, Cox said.

That ended a normalizing but still somewhat volatile 2023 with about half the decline the firm saw in 2022, but more than what’s seen in a typical year, said Jeremy Robb, senior director of economic and industry insights for Cox, during call with reporters this month.

Though prices have come down over the last two years, they are still about 33 percent higher than they were at the end of 2019, Robb said.

The fact that new-vehicle supply has returned to spring 2020 levels also should favor consumers and lead to lower vehicle prices, Cox Automotive Chief Economist Jonathan Smoke said during the call.

“This means we officially bid farewell to the seller’s market that has defined the last four years,” he said.

Affordability

There also remains the broader complication of affordability: New vehicles are increasingly more expensive, and higher interest rates continue to keep some shoppers wary of financing a vehicle.

Myers described how a Sons Auto Group customer ended an almost-closed sale in the dealership finance office when the buyer realized the loan interest rate would be 6.9 percent. Those scenarios did not happen two years ago when borrowing costs were lower, Myers said.

Germain’s Farkas said he is watching to see if customers being more conscious about their used-vehicle budgets will have a measurable impact on revenue — particularly on the F&I side.

“I feel people are still stretching for the car that they would like to have and F&I products might not fit in that budget as much as [they] used to in the past,” Farkas said.

Encouraging signs

Though the used-vehicle market is still challenging, there are some encouraging signs, CarMax Inc. CEO Bill Nash said during the company’s earnings call in December.

The return of more consistent used-vehicle price depreciation could attract budget-conscious customers who have been hesitant to buy, said Nash, who oversees the company that retailed the most used vehicles in the U.S. in 2022. If interest rates at least stabilize, that could be similarly useful, he said.

In its fiscal quarter that ended Nov. 30, CarMax reported an average used-vehicle sales price of a little more than $27,000. In its fiscal year that ended Feb. 29, 2020, that was $20,418. Nash said he thinks it’s possible for CarMax to get back to an average sales price in the mid-$20,000s. Though it’s unlikely prices fall all the way back to 2019 levels, there is “plenty of room” for adjustment, he said.

“Do I think they’ll get all the way there? I don’t think so, partly because new cars are becoming more and more expensive,” Nash said.

After big Tesla bet, Hertz selling one-third of EV fleet

Car-rental company cites low demand, says some proceeds to be used to buy internal-combustion-engine vehicles

Hertz is selling about a third of its global electric-vehicle fleet, a major reversal for the rental-car company after it positioned itself as a champion of the technology with plans to vastly grow its fleet of plug-in models.

HertzHTZ said Thursday that it would sell about 20,000 EVs in the U.S., and use some of the proceeds to purchase internal-combustion-engine vehicles. The company in a regulatory filing cited weaker demand for electrics, and their higher operating costs.

The move is the latest example of a swift retrenchment by the car business on EVs. After years spent outlining aggressive expansion plans, automakers in recent months have put some EV projects on ice and dialed back production forecasts, citing signs that U.S. consumers aren’t ready to move to cars powered exclusively by batteries as quickly as once thought.

The car industry’s effort to sell consumers more broadly on EVs has run into some resistance lately as automakers have largely exhausted the pool of early adopters who tend to be willing to take a chance on new technology.

EV sales in the U.S. increased last year but the pace of growth has slowed. Car buyers are worried there won’t be enough places to plug in or their travel will be too limited by battery range, surveys show. High prices also are turning off consumers.

Hertz signaled its big push into EVs in 2021, with a surprise move to eventually purchase 100,000 Tesla EVs. The Estero, Fla., company, which months earlier had emerged from bankruptcy, pegged part of its turnaround story to the effort to broaden electric choices for customers.

“Electric vehicles are now mainstream, and we’ve only just begun to see rising global demand and interest,” said Mark Fields, a former Ford Motor chief executive, who was then serving as Hertz’s interim CEO. Hertz’s stock rose 10% that day, and helped send Tesla’s valuation above $1 trillion for the first time.

At the time, Scherr said some of Hertz’s customers were eager to rent EVs to avoid high gas prices, and he added that nearly half of the company’s electric rentals had enough range that customers wouldn’t need to stop and charge. In September 2022, Hertz said it would buy 175,000 EVs from GM over five years.

Around then, automakers had been touting long wait lists for their newest electric models, and early buyers were shelling out thousands of dollars above the sticker price for them. Other rental companies, including Avis Budget Group, also signaled their interest in expanding their EV offerings.

Signs of a looming deceleration in the U.S. EV market appeared early in 2023, when Tesla sharply cut prices, pressuring other automakers that had been rolling out new EV models at the time.

Tesla’s price cuts last year lowered the starting prices of some models by about a third in the U.S., hammering the value of used Teslas and other electric cars, which began sliding in late 2022 and continued to decline throughout most of last year.

Hertz previously set a goal to electrify a quarter of its fleet by the end of 2024. On Thursday, the company said it would focus on matching supply with demand and focus on margins.

Hertz has faced higher repair costs on its EVs, and price cuts for Tesla cars have dented the value of its electrified fleet. The company said Thursday it would still offer EVs to customers and was working to improve profitability on its remaining fleet by expanding charging infrastructure and working with EV makers to access more-affordable parts.

The company said it would log a $245 million incremental net depreciation expense related to the sale of the 20,000 electric vehicles. Hertz sells its used rental vehicles directly on its website.

It expects to improve its bottom line by about that same amount over the next two years by replacing the EVs with internal-combustion-engine models.

Hertz on Thursday also cut its outlook for the year, in part from higher collision and damage expenses, primarily related to EVs, the company said.

It is forecasting adjusted Ebitda, or earnings before interest, taxes, depreciation and amortization, of negative $120 million to negative $130 million, not including the noncash charge related to selling electric vehicles.

Hertz said it is expecting revenue of $2.1 billion to $2.2 billion in the quarter ended Dec. 31, compared with $2.04 billion a year earlier. Analysts polled by FactSet are expecting fourth-quarter revenue of $2.19 billion.

Corrections & Amplifications Tesla recently had a market capitalization of nearly $750 billion. An earlier version of this article incorrectly said its market capitalization was nearly $750 million. (Corrected on Jan. 11)

Cars.com survey reveals surprising 2024 auto trends

The quest for an affordable ride goes way down market, a late-model trade-in that’s in good condition equals a major windfall, enthusiasm for battery electric vehicles is just, meh and, big surprise, kids want cars again.

Those are some of the trends emerging this year according a consumer survey by vehicle research and shopping website Cars.com.

Results are based on 4,000 responses to the survey taken between August 30 and September 7, 2023.

Overall vehicle affordability is an ongoing challenge for many consumers. The combination of low inventories caused by Covid pandemic production and supply chain interruptions, automakers’ preference to convert their product lines to high-profit pickup trucks and SUVs and a pullback on discounts had average transaction prices shooting up to around $50,000.

That’s more than sticker shock. It’s a disqualifier for shoppers on more modest budgets, many of whom now find themselves chasing a windmill that’s closer to a mirage.

“Our survey showed almost half of consumers are planning on spending $30,000 for a new car, but only about 12 percent of new cars are priced at $30,000,” said Rebecca Lindland, director, auto data and insights director at Cars Commerce, the Cars.com parent company, in an interview.

With such a paucity of more budget-friendly vehicles, Lindland suggests consumers concentrate less on the sticker price and more on the total picture.

“Go into your car shopping journey understanding what payment you’re comfortable with, understanding what size vehicle you need, really knowing your requirements and then not overspending, because just like, there’s nothing worse than being house poor, there’s nothing worse than being car poor,”Lindland advised.

It’s also vital, she said, shoppers understand the value of the vehicle they’re trading in. Right now, trade-ins are pulling in lucrative offers because quality used cars are in short supply.

“There’s a shortage of specifically one to five-year-old vehicles,” said Lindland. “But the silver lining is that if people are trading in a vehicle from one to five years old, it’s actually worth almost 23percent more than it would have been in 2020.”

The downside, she warned, is high prices paid by dealers for trade-ins also mean high prices for those shopping for a used car or truck.

There is some evidence prices for some vehicles are moderating. Now that new vehicle production is working its way toward pre-pandemic levels and dealer inventories are growing, consumers have more choices and automakers are more likely to resume discounting.

Indeed the new-vehicle average transaction price in December 2023 was $48,759, an increase of 1.3 percent month over month but down 2.4 percent year over year, according to Kelley Blue Book.

Earlier this week Cox Automotive chief economist Jonathan Smoke declared the end of the seller’s market.

Pricing remains, however, a barrier to some for making the switch to a battery-electric vehicle. That doesn’t mean consumers aren’t concerned about reducing dependency on fossil fuels or protecting the environment, they’re just not ready to go all-in on EVs.

Their fallback plan, for now at least, are hybrids and plug-in hybrids which provide higher fuel economy using a combination of a gasoline engine, electric motor and battery pack. A plug-in hybrid adds the capability of plugging in the vehicle’s battery to recharge it.

Hybrids are not generally as costly as pure EVs and consumers are noticing that. About twice as many are people researching and shopping for hybrids and plug-in hybrids versus a full electric vehicle on Cars.com, according to Lindland.

A key issue, aside from price and charging concerns, she maintains, is the inadequate job being done by the federal government and automakers in communicating how far EVs have come.

“We need to work on the story to say an electric vehicle is such a great vehicle for so many applications, especially now that people are working from home or they’re not commuting this much,” Lindland asserted. “The range has expanded dramatically and you can get an EV that you can drive for hundreds of miles without needing to charge it. Even charging has improved so dramatically so you’re not sitting there for 24 hours anymore. With the level three charger you can charge in half an hour.”

Regardless of what powers a vehicle Millennials, those born between 1981 and 1996, largely preferred not to own one, opting to get around via rideshare or public transportation.

But those born between 1997 and 2012 who make up what’s known as Gen Z, are more open to owning their own rides after seeing that grabbing an Uber or Lyft isn’t necessary a panacea according to Lindland.

Forty-two percent of Gen Zers bought their first vehicles between ages 16 and 18 compared with 32 percent of Millennials, according to Cars.com research.

Not only are they buying earlier, their method for doing so represents a shift.

“The fascinating part that I found really interesting is that 80 percent of the Gen Zers that we surveyed said I want to finish my transaction at the dealership, which I find just wild. Wow. It’s so illogical, but I think they want that authentic experience,” said Lindland. “I think they want to look the person in the eye and understand who they’re buying from, what kind of a deal they’re getting and they want that handshake. They want that human connection.”

Lindland stresses that no matter what price or powertrain vehicle a consumer is shopping for, and regardless of whether it’s new or used, the tools to find the right ride at the right price are free and easy to find online, adding, “There’s so much information out there, and it’s just worth it to do some research.”

Car sales slow as U.S. buyers suffer sticker shock

US auto sales softened at the end of last year as higher financing costs and near-record prices took their toll on would-be buyers.

Pent-up demand that propped up sales in the wake of the pandemic has been sated, and shoppers are now balking at 10 percent interest rates on car loans and average prices around $48,000. Sales likely slipped to a seasonally adjusted annual rate of about 15.4 million vehicles in the final month of 2023, down from about 15.5 million in the prior two quarters, according to estimates compiled by Bloomberg.

“We’ve seen a big reduction in median- and lower-income households” buying new cars, which now “almost exclusively go to the top 20 percent of income households,” Jonathan Smoke, chief economist for researcher Cox Automotive, said in an interview.

While 2023 was a marked improvement over an inventory-constrained 2022, the challenges seen at the end of the year are expected to persist. Cox Automotive predicts US auto sales will be up less than 2 percent in 2024. That means the figure is unlikely to top 17 million anytime soon, as they did for five consecutive years prior to the pandemic.

“The new norm for the industry because of reduced affordability is closer to 16 million,” Smoke said. “We’ve lost about 10% of the buying pool.”

Automakers aren’t motivated to cut prices because they’re making more money selling fewer cars. Consumer spending on new vehicles reached a record $578 billion in 2023, its third consecutive year exceeding a half-trillion dollars, according to researcher J.D. Power. Consumers’ average monthly car payment in December was estimated to be $739, up $9 from a year earlier, J.D. Power said.

“Unless the industry finds a way to get back to more-affordable price points, we will see products that cater to higher income, higher credit-quality consumers,” Smoke said. “And that ultimately limits sales volumes.”

How electric vehicles are losing momentum with U.S. buyers, in charts

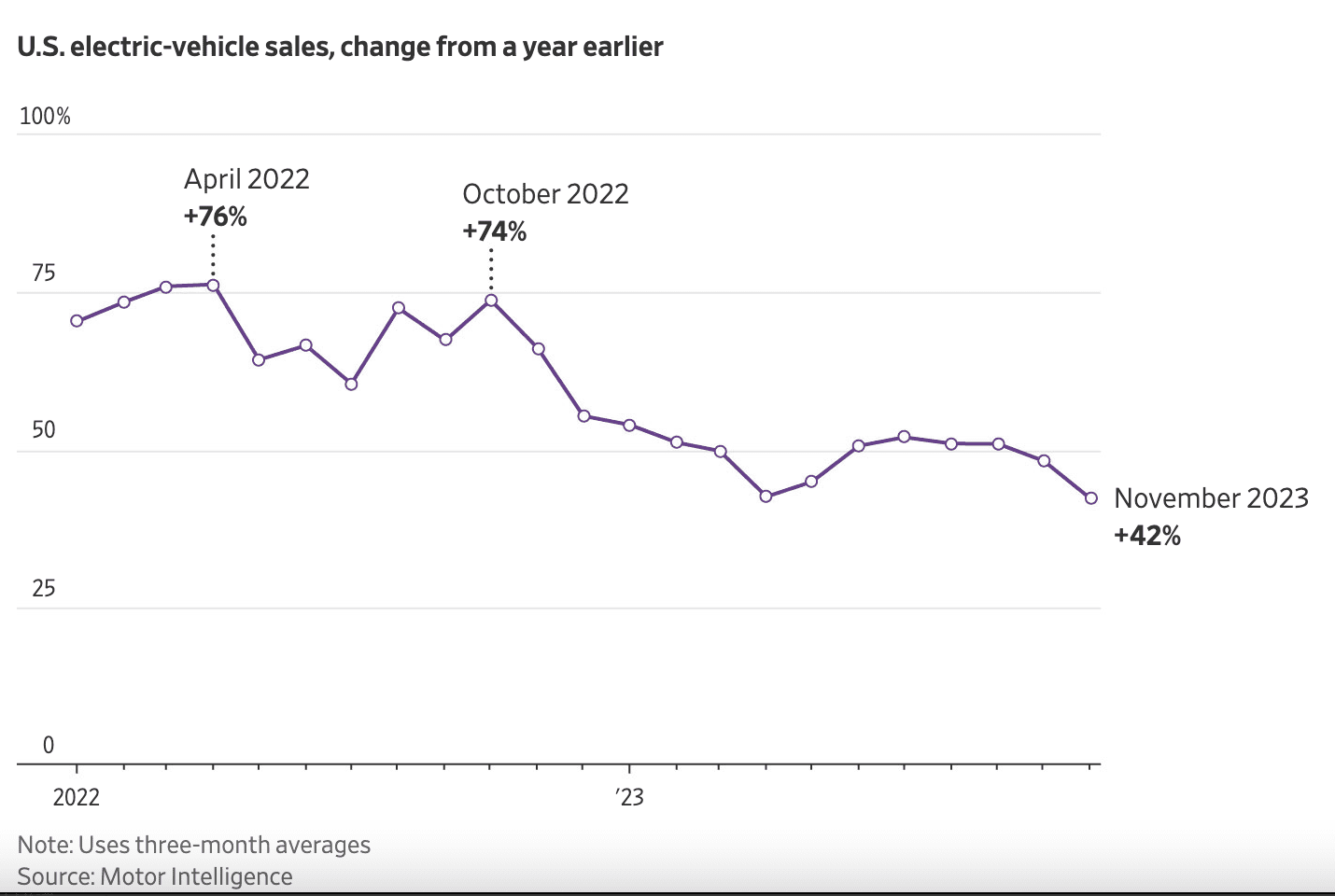

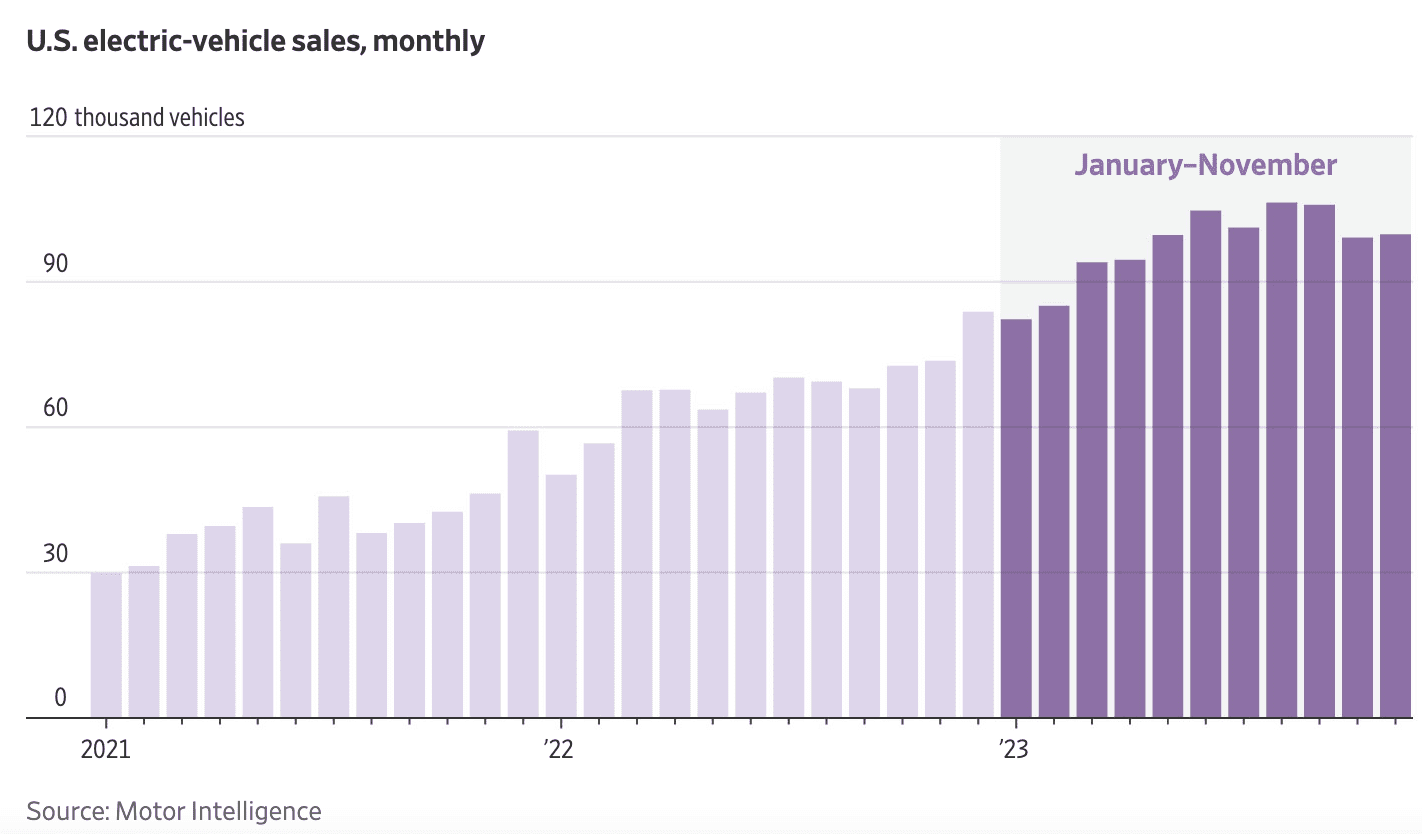

EV sales grew nearly 50 percent this year but have plateaued in recent months

Electric-vehicle sales growth hit a speed bump in the U.S. this year, and the impact is being felt throughout the industry.

Carmakers around the world have invested billions of dollars in EV technology, spurred on by tailpipe emissions regulations designed to boost sales of battery-powered models. But as customers in the U.S. hesitate to make the switch from traditional gas-engine vehicles, some auto companies are delaying plans on electric-vehicle spending.

Sales of electric models rose rapidly in the first 11 months of the year, faster than the car market as a whole but at a slower pace than in previous years.

Car executives say they are confident that sales will accelerate as additional lower-priced models come out and the availability of public chargers improves.

In the near term, the cooling buyer interest has weighed onU.S. makers that had ramped up vehicle and battery production in anticipation of a larger surge in customer demand. Electric-vehicle sales began to stall in the latter half of this year, a move that car executives attributed to the relatively high prices of electric models.

As a result, electric cars and trucks are piling up on dealer lots, causing auto companies to reassess their investment plans.It takes a dealership around three weeks longer to sell an EV than a gasoline vehicle, according to data from car-shopping website Edmunds. A year ago, battery-powered models were selling faster than their gasoline counterparts.

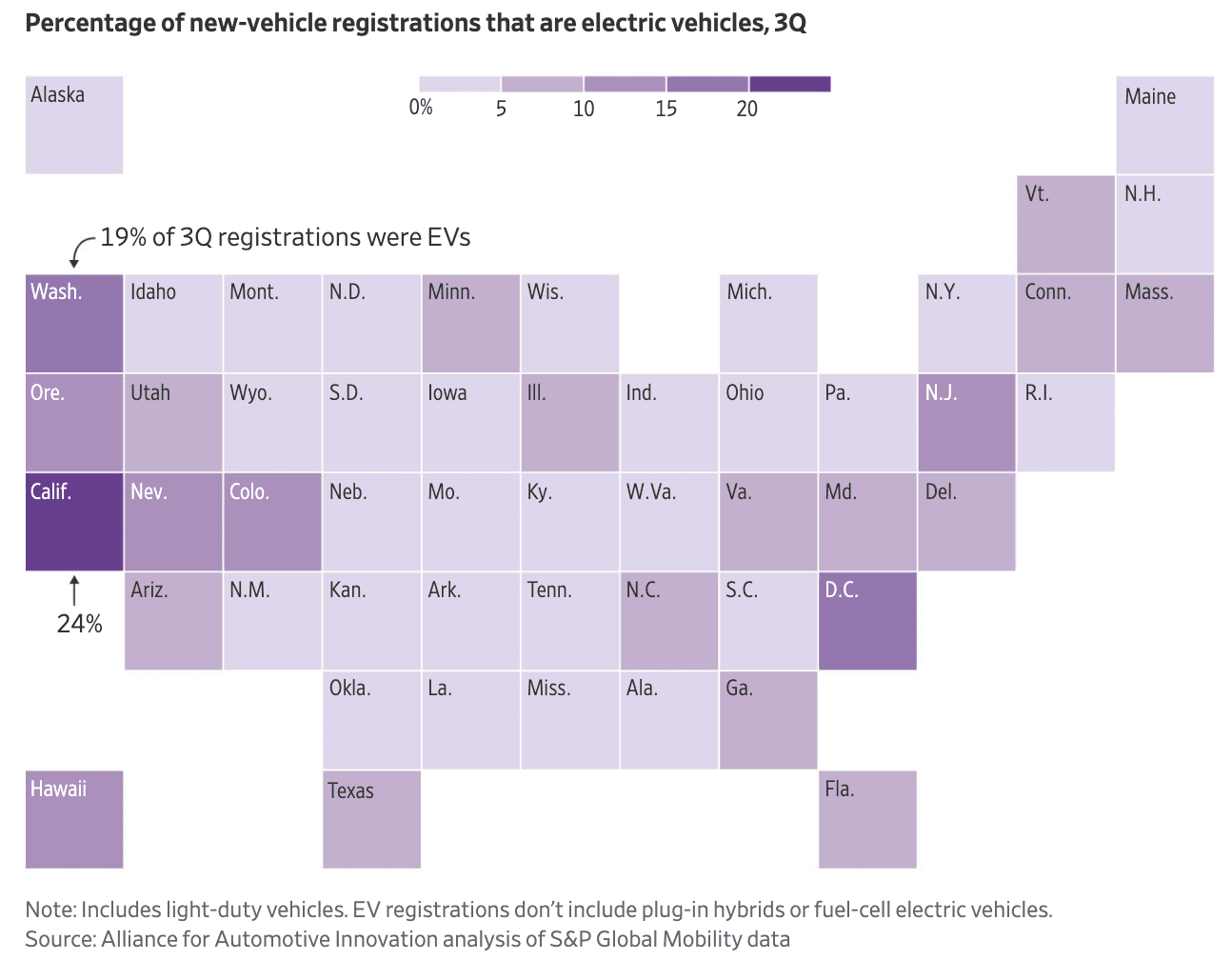

Part of the challenge for automakers is that demand for electric models isn’t spread evenly across the U.S. Sales are concentrated in a handful of states, according to data from S&P Global Mobility.

Between July and September, nearly a quarter of all vehicles sold in California were EVs, compared with a little over 3 percent inMichigan where General Motors and Ford Motor have their headquarters, according to the trade group Alliance for Automotive Innovation, which analyzed data from S&P Global Mobility. Most buyers are in urban areas, where public charging infrastructure is more readily available, say dealers and car executives.

Through September, six of the top 10 car markets for electric cars and trucks were cities on the West Coast, and the top four were metropolitan areas in California, according to S&P Global Mobility.

Dealers and carmakers say many American car buyers are still reluctant to ditch their gas vehicles for an electric model, put off by the relatively high price of the technology and concerns about their ability to recharge them easily.

Automakers are offering a combination of discounts and lower interest-rate deals in an attempt to draw in buyers. Those markdowns have led to a sharp decline in new EV prices and an even steeper decline for their counterparts in the used-vehicle market.

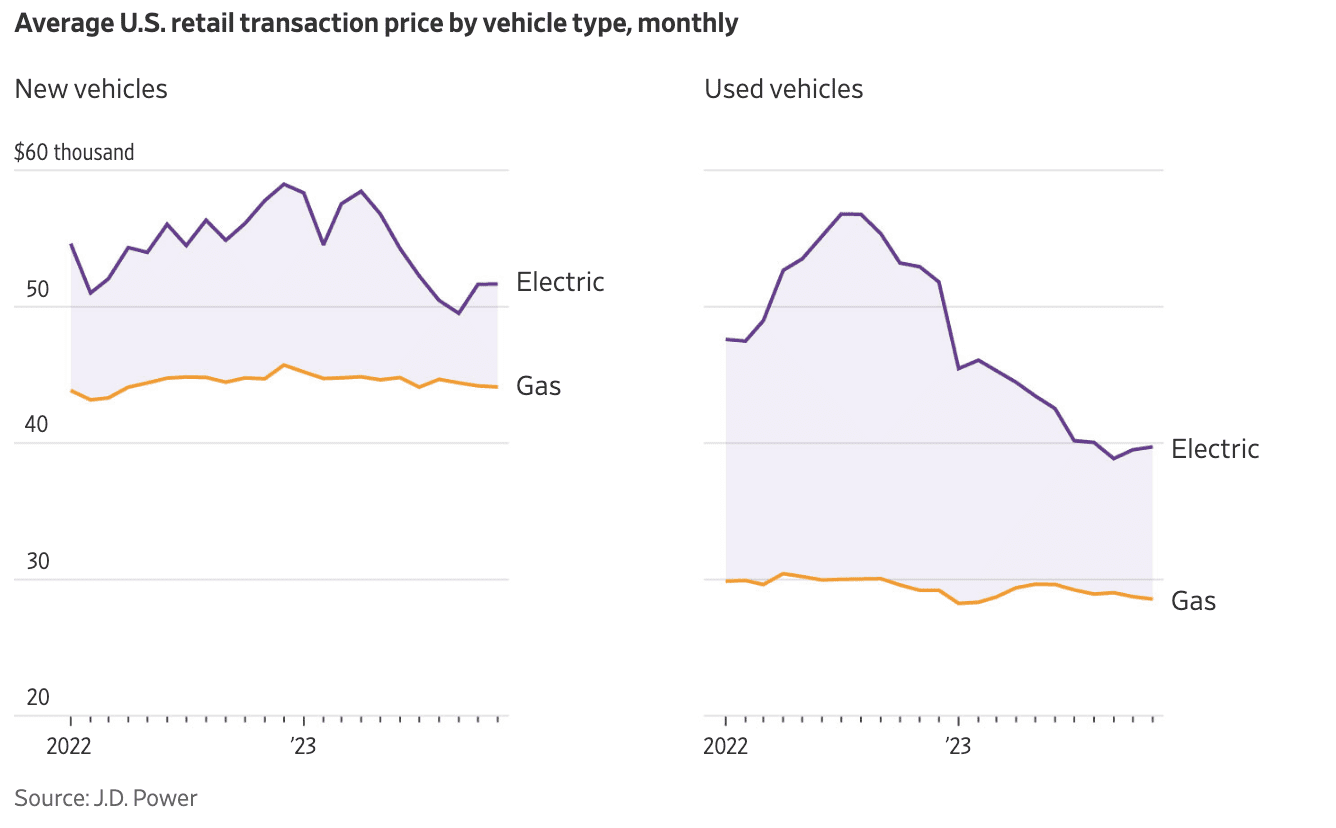

American car buyers paid $51,668 for a new EV in November, compared with $44,112 for a newgasoline-powered model, according to J.D. Power data.

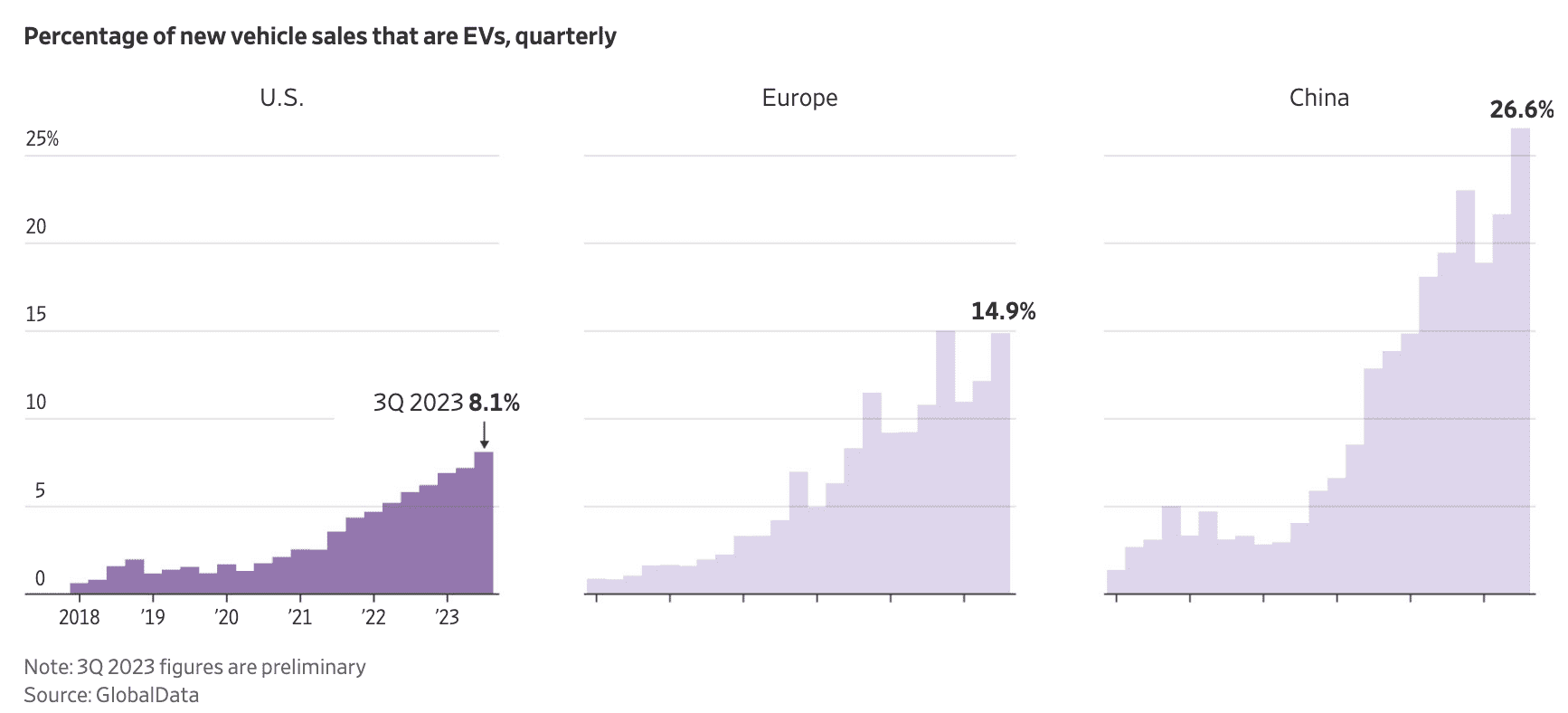

Electric-vehicle sales in the U.S. have been slower to take off compared with the world’s other two large car markets: China and Europe. Nearly 27% of the vehicles sold in China were battery-powered models in the third quarter, compared with around 8% in the U.S., according to preliminary data from research firm GlobalData. In Europe, nearly 15% of the vehicles sold in the third quarter were EVs.

Analysts say that trend is partly caused by China and Europe moving earlier and more aggressively to promote sales of electric vehicles with a combination of government subsidies and tougher emissions regulations. Analysts say that the U.S., as a relative latecomer, needs more time for car companies to release more electric models and for consumers to become comfortable with the technology.

Auto executives and analysts say that a lack of affordable models is preventing electric-vehicle sales from taking off in the U.S., but that this is likely to change in 2025, when lower-priced options are expected to become available.

“We’re going to start to see more of these EVs under $35,000 to $40,000,” said Stephanie Valdez Streaty, an analyst at automotive services company Cox Automotive. “It’s a major transition. It will go forward, but there will be major bumps and zigzags.”